- 繁体中文

- 简体中文

- English

- Español

- Tiếng Việt

- Português

- لغة عربية

- ไทย

分析

However, upon reflection, the meeting feels somewhat more consequential than the ‘copy and paste’ nature of the statement, and press conference remarks, would imply.

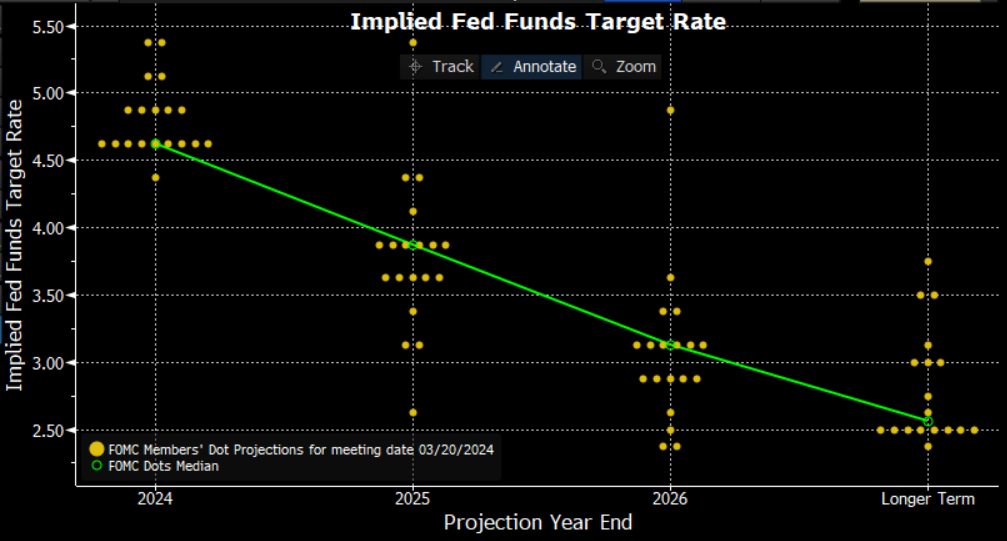

There are two key metrics, both within the latest SEP, that send this message.

The first is the aforementioned ‘dot plot’, with the median expectation among FOMC members still being for three 25bp rate reductions over the remainder of 2024. The second, also within the SEP, is the latest inflation forecast, with expectations for the Committee’s preferred price gauge – the core PCE deflator – having been nudged 0.2pp higher to 2.6% this year, with a return to the 2% target still only being foreseen in 2026, using either the headline or core measures.

In other words, the FOMC now expect inflation to be higher than previously thought this year, but still expect to deliver the same amount – 75bp – of rate cuts. Clearly, this is a Fed that is desperate to get on with normalising policy, and slowly removing restriction from the economy.

The FOMC’s language, and that of Chair Powell, also helps to stress this point. While the policy statement makes clear that the Committee are seeking additional data to confirm that disinflationary trends are well-embedded within the economy, the first rate cut is provisioned on inflation moving “toward” the 2% target, and not inflation actually hitting that magic number.

Other G10 central bankers have also sent a similar message of late. BoE Governor Bailey, for instance, was explicit in noting that the MPC “don’t need to see inflation at 2% before acting”, while the ECB are all-but-certain to deliver a June rate cut, despite the March round of staff macroeconomic projections not expecting the 2% inflation target to be achieved until the third quarter of 2025.

Of course, some caveats are needed here. The path back to 2% inflation, particularly the last mile of said path which we are now well within, is indeed proving bumpy, with particularly services prices remaining at stubbornly high levels. Furthermore, as inflation does recede, were nominal rates to remain unchanged, this would obviously see real rates move higher, making the overall policy stance more restrictive, potentially choking growth, and throwing into doubt the ‘soft landing’ that, in particular, the US economy looks on course for. Some degree of cuts, then, is necessary simply in order to ensure that the relative stance of monetary policy does not unnecessarily tighten.

However, the comfort, and some may say hurry, that policymakers have displayed with delivering rate cuts even with above-target inflation, suggests that the 2% goal may soon be about to become a floor, rather than the ceiling that it was in the pre-pandemic economy. In other words, the explicit 2% price target may well be quietly forgotten by policymakers, with a range above that figure instead being targeted.

The net effect of this was also hinted at in the March SEP. While the FOMC’s 2024 median dot remained unchanged, the 2025 & 2026 dots each nudged higher by 25bp, while the ‘longer-run’ rate expectation (i.e., the FOMC’s estimate of neutral) also rose to 2.56% from 2.5% prior, with just one, compared to three, members now seeing a neutral rate below that 2.5% level.

Put simply, policymakers being happy to sanction higher inflation in order to get on with policy normalisation sooner rather than later will likely lead to the easing cycle being somewhat shallower and shorter than had been expected (barring financial accident), thus resulting in higher long-run rates, and a steeper Treasury curve, particularly as the front-end rallies as rate cuts are delivered.

Importantly, though, although the FOMC, and others, look set to tolerate higher inflation, market-based inflation expectations remain well-anchored; though, using US breakeven rates, both 2- and 5-year rates point towards an inflation band being targeted, as outlined above, rather than pointing to expectations of a return back to precisely 2%.

All the while that inflation expectations remain well-anchored, implicitly targeting a higher range for actual inflation is unlikely to pose significant issues, and in fact represents the late-cycle economic reality where prolonging growth, and importantly – especially, in a US election year – maintaining a tight labour market, begins to outweigh the other side of the Fed’s dual mandate. However, such a strategy does leave relatively little ‘wriggle room’, and exposes the risk of expectations becoming unanchored, particularly in the event of an adverse supply-side shock, a risk that remains present given the fragile geopolitical landscape.

This, subsequently, raises the question of what the cross-asset market implications of all this may prove to be.

In the FX space, where some tentative signs of policy divergence, and thus volatility, have begun to re-emerge, the story is likely to remain much the same as it is at present.

Namely, where the delivery of early, and deeper, rate cute sparks FX weakness, while a ‘higher for longer’ rate path sees the respective currency benefit from a wider yield differential vs. peers. In light of this, downside risks seem most significant for the CHF, EUR, and SEK, while the USD should continue to gain relatively broadly against peers. The BoJ’s rate hike campaign, which has just got underway, is only likely to see a very limited degree of tightening delivered, and unlikely to diminish the JPY’s place as an attractive funder within G10.

In contrast, the implications of an inflation band being targeted, and thus the likelihood of longer-run rates being higher, is more difficult to gauge in the equity space.

Textbooks would dictate that a hawkish reassessment of policy expectations should pose a headwind for riskier assets. However, at risk of falling into the ‘this time is different’ trap, that may not prove to be the case in the current environment, particularly when one decomposes the rationale as to why major US indices – and, incidentally, their global peers – trade to fresh record highs, having rallied strongly this year.

_YTD_st_2024-03-24_14-46-54.jpg)

The key concept to understand here, in my view, is that the YTD rally is built on what policymakers can do, and not necessarily what they will do.

Whether the Fed deliver the first cut in June, July, or in the autumn matters relatively little in practical terms over the medium-run. The same is true of the timing of other G10 central bank cuts, and of when said policymakers also reach consensus on, and bring to an end, the various balance sheet run-off programmes currently in place.

What matters is that, as discussed, with inflation now back at what policymakers deem to be a level acceptably close to target, they are able to deliver significant easing, a faster end to balance sheet run-off, and even resume liquidity injections (targeted or otherwise), if the economy were to require it. In layman’s terms, the central bank ‘put’ that markets enjoyed during the post-GFC era, and which went away post-covid during the battle against double-digit inflation, is now back in place – alive, well, and nimbler than before.

This must be coupled with recent evidence from the equity market that stocks, particularly those megacap in the tech sector, have been able to deliver, and even surpass, earnings expectations in both rising and falling inflation environments. Furthermore, as has been extensively discussed, the typically negative equity-bond correlation has also weakened significantly in recent times, particularly during this cycle.

These two factors combined should see investors remain comfortably with increasing exposure to risk, and leave the path of least resistance pointing higher for global equities, albeit with that path perhaps being a tad narrower than if a precise 2% inflation goal were still being targeted.

Related articles

Pepperstone不代表這裡提供的材料是準確、及時或完整的,因此不應依賴於此。這些資訊,無論來自第三方與否,不應被視為建議;或者買賣的提議;或者購買或出售任何證券、金融產品或工具的招攬;或參與任何特定的交易策略。它不考慮讀者的財務狀況或投資目標。我們建議閱讀此內容的讀者尋求自己的建議。未經Pepperstone的批准,不允許複製或重新分發此信息。