- 繁体中文

- 简体中文

- English

- Español

- Tiếng Việt

- Português

- لغة عربية

- ไทย

分析

February 2024 US CPI Preview: The Final Piece Of The Pre-FOMC Data Jigsaw

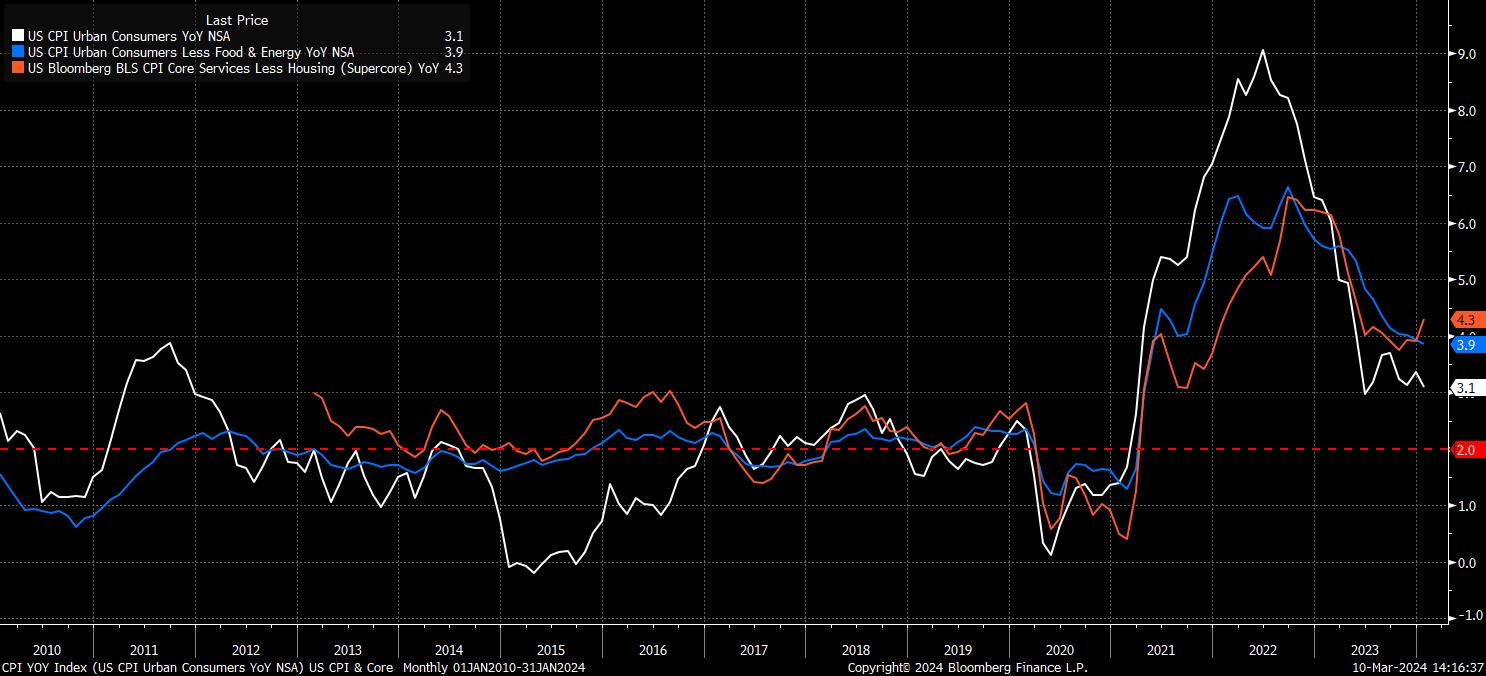

Off the back of hotter than expected inflation figures in January, with price pressures in the services sector remaining particularly stubborn, consensus sees headline CPI remaining unchanged at 3.1% YoY in February, though the core measure should cool 0.2pp, to 3.7% YoY. On an MoM basis, headline CPI is seen quickening to 0.4%, from 0.3%, while the opposite is true of the core figure, set to cool to 0.3% MoM from the 0.4% pace notched in January.

Clearly, while data in line with consensus would again point to inflation remaining more elevated than most would desire, particularly those on the FOMC, such a report would at least point to the fact that underlying inflationary trends don’t appear to be strengthening. While this may seem like ‘clutching at straws’, it’s important to recognise that policymakers are not overly focused on a single month of data, instead paying much closer attention to the trend that inflation is taking over a period of time.

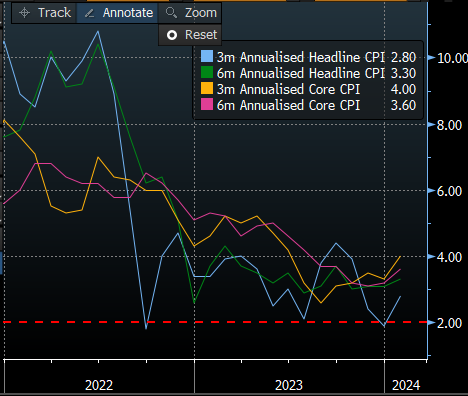

On this note, it is the 3- and 6-month annualised rates of core CPI that are likely to be the most closely watched areas of the report. This is especially true given the pickup in the former gauge to 4% last month, its highest level since last June, implying that it may still be some time before the FOMC have the “confidence” in a return to the 2% inflation target that they are seeking before delivering the first rate cut.

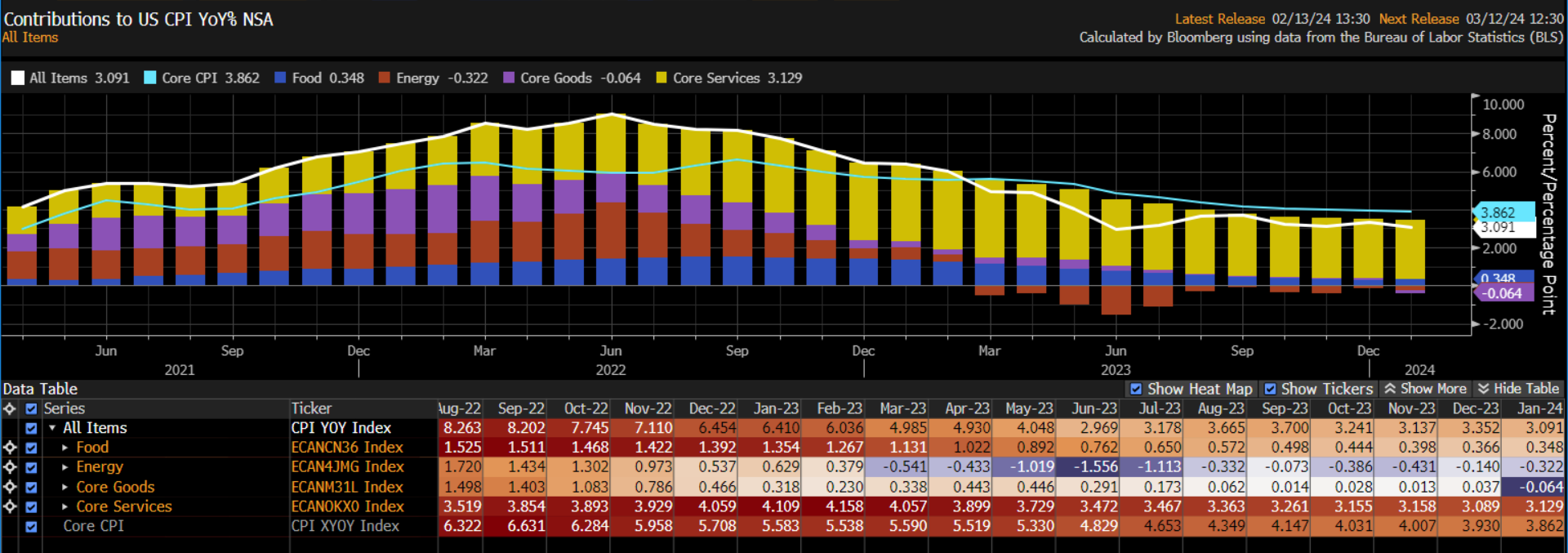

In terms of the details of the inflation report, the data will likely again flag deflation in goods, with the core services category still providing the most significant inflationary impulse, and being the main hurdle to achieving a further easing in price pressures.

There are, however, some quirks with the data here, particularly in terms of shelter, with the ‘Owners Equivalent Rent’ (OER) measure accounting for around a third of the core CPI figure. Without digging into the weeds too much, the surge in OER in the January report, primarily due to the BLS re-weighting their sample for calculating the measure, played a significant role in the substantial upside surprise in the core CPI metric. With single-family detached homes now having a higher weight in the OER index, and rent inflation here outpacing that of other housing categories, OER is likely to remain elevated for some time, somewhat underpinning the core CPI metric.

Furthermore, this will likely lead to a continued divergence between the more widely-watched CPI figures, and the Fed’s preferred PCE inflation gauge. OER comprises only around 15% of the core PCE figure, less than half its weight in the core CPI metric, thus raising the risk of drawing false conclusions on the policy outlook by looking at the consumer price index alone.

In any case, data quirks or not, the February CPI report is likely to be a significant vol event for financial markets, particularly with it representing the final top-tier data point due before the March FOMC decision. Incidentally, with us now being just over a week from that meeting, the Fed are now in the pre-meeting ‘blackout’ period, meaning there will be no comments from policymakers in the aftermath of the inflation figures, somewhat leaving investors ‘flying blind’ as to how the Committee may interpret the data when they meet for their next confab.

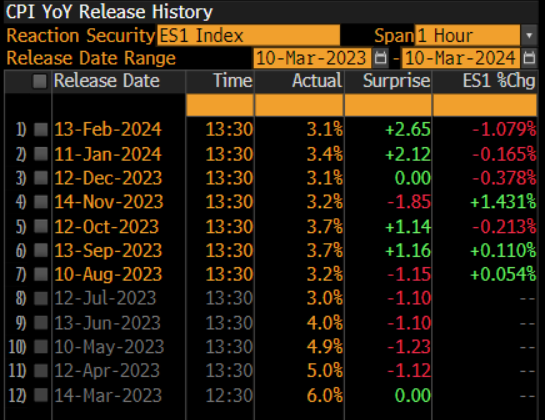

As a somewhat rough form guide, we can examine how markets have reacted to CPI prints in recent months, of course remembering the key caveat that past performance is no guarantee of future results.

Over the last year, the S&P 500 has ended the day in negative territory on just four occasions on ‘CPI Day’, with the average move in the benchmark index standing at +/-0.8% over the last six months on the day of the inflation release, the highest said average has stood at since April.

Condensing the timeframe further, the front S&P 500 future has fallen in the 30 minutes, and the hour, following the CPI release on the last 3 occasions, with an average decline of 0.6% and 0.5% over each period, respectively. It must be said, however, that the last 2 headline YoY CPI figures did surprise 0.2pp above consensus expectations, perhaps skewing this study somewhat.

Unsurprisingly, the opposite of the above study is true if one looks at the performance of the dollar, using the DXY as a relatively rudimentary proxy. The greenback has gained ground in the hour following the CPI print on 4 of the last 5 occasions, with each of these 4 rallies following a hotter-than-expected inflation figure.

It seems logical to expect that playbook to again hold true this time around, with cooler-than-expected data likely to spark a dovish reaction (risk bid, Treasuries rally, USD sold), and hotter-than-expected figures likely to ignite a hawkish one (USD bid, risk sold, Treasuries offered). As alluded to, the core MoM print is likely the most significant in terms of prompting a short-term market reaction

Any dovish reaction, though, is unlikely to see markets bring forward pricing of the first 25bp Fed cut to May, from June, with one positive inflation surprise likely being far from enough to provide the FOMC with the “confidence” needed that inflation is on its way back to the 2% target.

In fact, from a policy point of view, one inflation report – no matter if hot or cold – is unlikely to dramatically alter the thinking of most policymakers on the FOMC, with rate cuts this year still overwhelmingly likely. What a trend of hotter-than-anticipated data may trigger, however, is a reassessment of how many cuts will be delivered this year, and when they may begin.

On this note, a hot report will substantially raise the probability of the median 2024 dot, in the FOMC’s March SEP, pointing to 50bp of easing this year, compared to the present 75bp median; it will only take two policymakers moving their ‘dot’ higher to shift the median to that extent, with that possibly being the biggest risk for equities at this juncture.

Related articles

Pepperstone不代表這裡提供的材料是準確、及時或完整的,因此不應依賴於此。這些資訊,無論來自第三方與否,不應被視為建議;或者買賣的提議;或者購買或出售任何證券、金融產品或工具的招攬;或參與任何特定的交易策略。它不考慮讀者的財務狀況或投資目標。我們建議閱讀此內容的讀者尋求自己的建議。未經Pepperstone的批准,不允許複製或重新分發此信息。