- 简体中文

- English

- 繁体中文

- Español

- Tiếng Việt

- ไทย

- Português

- لغة عربية

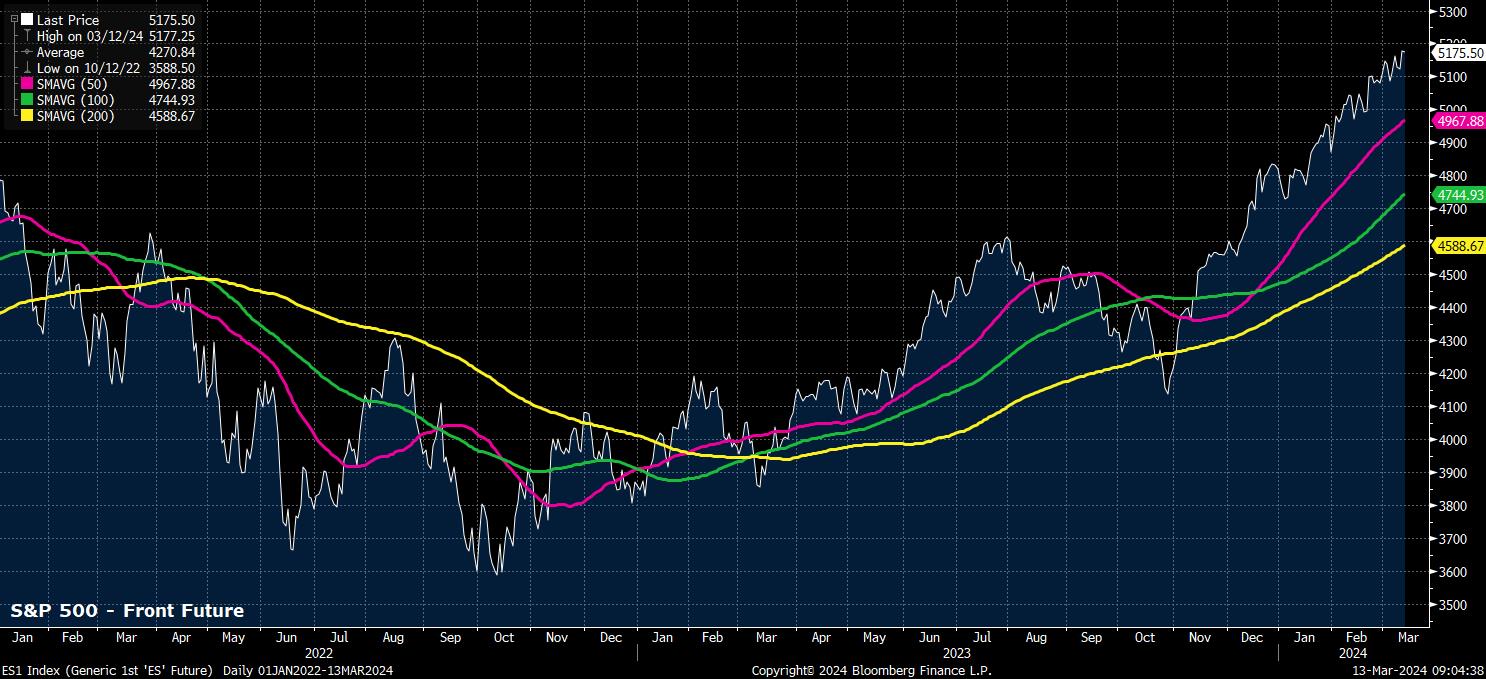

As noted, the upcoming FOMC decision is highly unlikely to result in any significant shifts in the policy stance. Consequently, the target range for the fed funds rate is all but certain to remain at 5.25% - 5.50%, in what should again be a unanimous vote, with money markets implying no chance of any rate move at this meeting.

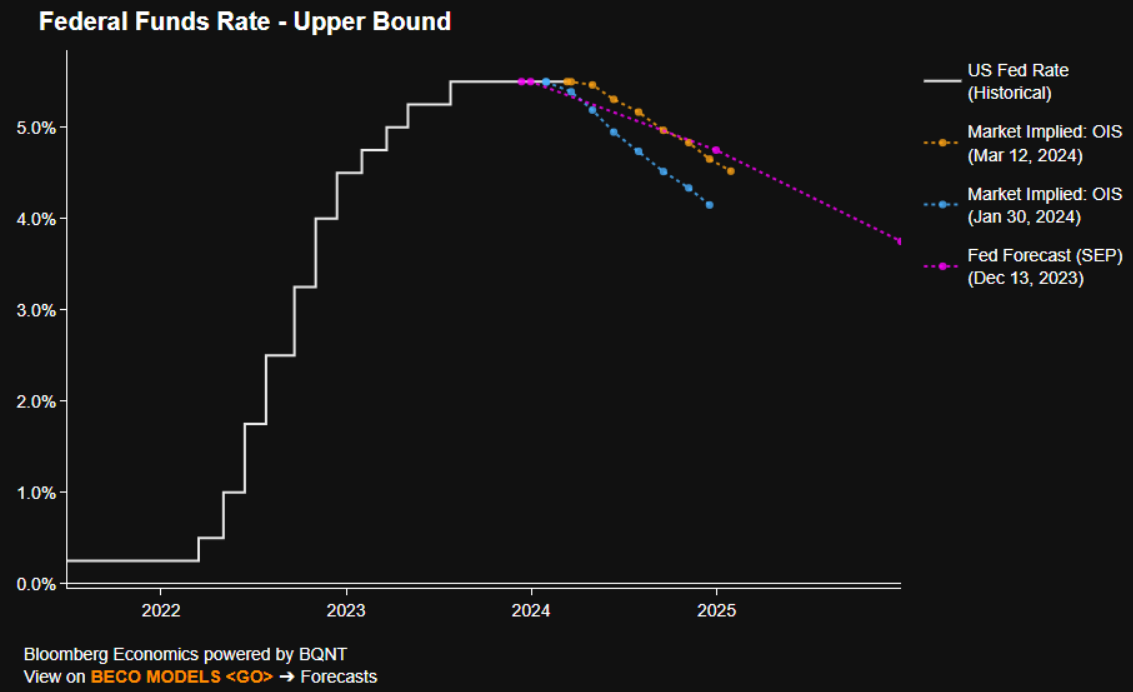

Looking further along the USD OIS curve, and markets continue to price what is likely to be a ‘summer of easing’, not only from the FOMC, but also from the majority of other G10 central banks. Currently, markets imply around a 4-in-5 chance that the Fed will deliver the first 25bp rate cut at the June meeting, with said move fully priced by July, in addition to a total of 83bp of easing being priced over 2024 as a whole.

This pricing represents a significant shift from where OIS was positioned prior to the last FOMC meeting back in January. Then, markets were fully pricing the first cut for May, while also expecting a total of 135bp of easing this year, implying around a 40% chance that the Committee would cut six times by December.

Clearly, these dovish expectations have been substantially pared back, with the OIS curve now – as near as makes no difference – pricing an outlook in line with that of the median 2024 dot from the December SEP, by virtue of hotter-than-expected jobs, and inflation, figures in the first couple of months of the year. With this in mind, and with the economy continuing to evolve broadly in line with expectations, there seems little reason for the Committee to substantially alter its present forward guidance, in that any “adjustments” to the fed funds rate will remain dependent on incoming data, and that rate reductions will only begin upon gaining “greater confidence that inflation is moving sustainably toward 2 percent”.

Note that said guidance would be, in broad terms, a repetition of that issued in January, where the FOMC explicitly pivoted to a more neutral stance on the policy outlook. There is little in the data, nor market pricing, to justify another step towards more explicitly dovish guidance at this juncture.

Despite that, there may be some other modest tweaks to the statement, though these should be relatively insignificant in the grand scheme of things. It now seems slightly unreasonable, for instance, to describe job gains as having “moderated” since early last year, particularly with – even accounting for a sharp downward net revision in the prior jobs report – headline payrolls growth having exceeded 200k for three straight months, and with the 3-month moving average of job gains now standing at +265k, its highest level since last June. Economic activity, meanwhile, is again likely to be described as expanding at a “solid pace”, while inflation continues to ease, but remains “elevated”.

In light of this largely unchanged economic outlook, the updated ‘Summary of Economic Projections’ (SEP) seems likely to be close to a ‘carbon copy’ of that delivered three months prior, broadly pointing to a ‘soft landing’ for the US economy.

Hence, the FOMC’s median real GDP growth expectations are likely to remain largely unchanged from the picture painted in December, perhaps with a modest upward revision to the 2024 forecast of 1.4% growth in reflection of continued resilience in the services sector, and amid signs that manufacturing output likely bottomed towards the latter part of 2023.

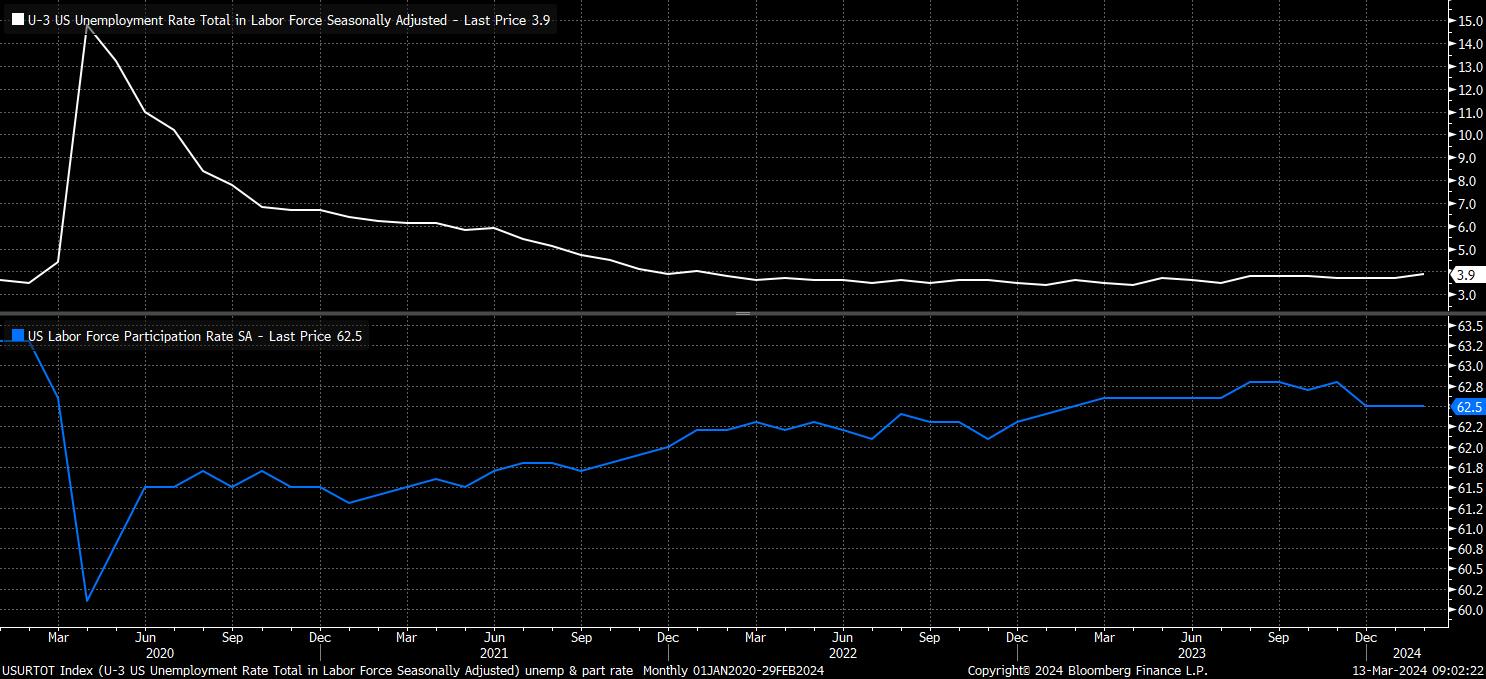

Similarly, labour market expectations are also likely to remain similar to those outlined in the last forecast round, despite a surprising rise in headline unemployment to 3.9% in the February jobs report.

It seems too early to extrapolate a trend from one month of data, though FOMC officials will naturally continue to interrogate the figures closely. Nevertheless, given the relatively resilient growth backdrop that is again likely to be outlined, and taking into account the fact that labour force participation remains around 0.3pp below the cycle highs seen in Q4 23, it seems reasonably to expect that any rise in joblessness will be relatively modest in nature, even though some degree of labour market loosening will likely be required in order to tamp down on sticky services inflation.

In sum, the current expectation of 4.1% unemployment through the end of the forecast horizon in 2026 continues to look reasonable.

Finally, on inflation, while risks to the current forecasts are tilted to the upside, any significant revisions to expectations that both headline and core PCE will rise 2.4% this year, with said rise moderating (in both gauges) to 2.0% by 2026, seem unlikely.

This is despite three straight hotter-than-expected CPI prints, primarily due to differences in the composition of the baskets used to calculate each measure. This centres most notably on shelter, with the ‘Owners Equivalent Rent’ (OER) measure accounting for around a third of the core CPI figure, and having been significantly skewed in recent months by calculation issues, mainly centred around the BLS re-weighting the sample used to calculate said measure, which has played a substantial role in the recent upside CPI surprises.

The Fed’s preferred gauge of price pressures, the PCE index, however, places a much lower emphasis on shelter prices, with the OER measure accounting for roughly a sixth of the basket here. In short, this should lead to much less of an inflationary effect in the PCE figures, thus increasing the likelihood that the forecasts remain unchanged, despite the recent hot CPI data.

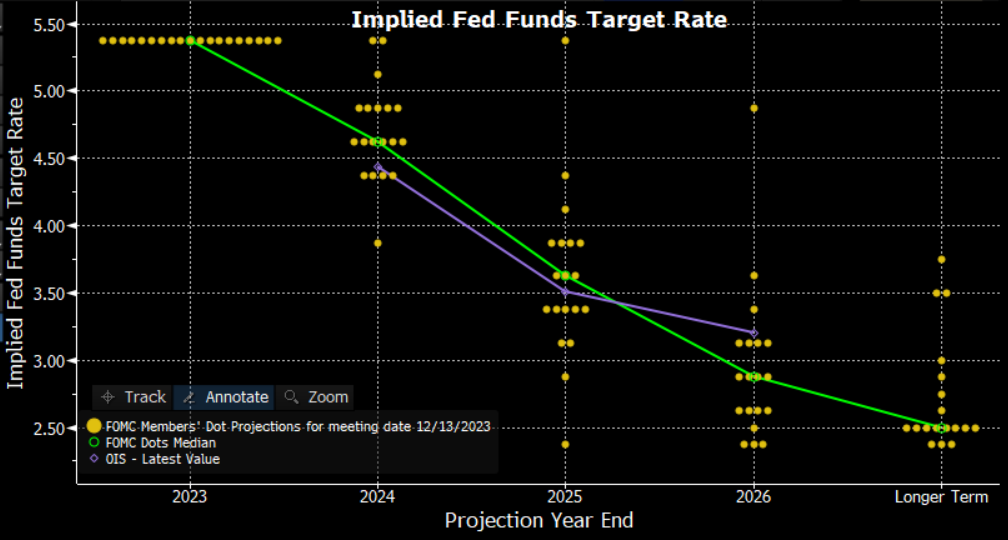

Tying all of this together, and in reflection of the relatively unchanged economic outlook, it seems logical to expect that the FOMC’s ‘dot plot’ will also be largely similar to that released in December.

As a result, the median expectation for the fed funds rate should again sit at 4.625% in 2024, implying 75bp of cuts this year, before a further reduction to 3.625% in 2025, and 2.875% in 2026, with the long-run fed funds rate expectation again likely to be pinned at 2.5%. Despite the likely unchanged outlook, it will be interesting to see whether the dispersion in the dots (with the current range of 2024 expectations from 3.875% to 5.375%) has tightened, often something that is interpreted as policymakers possessing an increasing degree of confidence in the baseline economic outlook.

Naturally, there are risks to this view. Principally, in that it would only take two policymakers presently aligned with the median expectation to revise their ‘dot’ 25bp higher, for the median to move by the same magnitude; while recent Fedspeak hasn’t seen any Committee members hint at such a scenario, the tight jobs market, and bumpy disinflationary path, mean it cannot be ruled out.

Furthermore, the longer-run fed funds rate estimate is also likely to provoke some interest, particularly after comments from voting (albeit retiring) member Cleveland Fed President Mester that she is considering raising said forecast. While such a view does not appear to have become a majority view on the FOMC at this stage, the pencilling in of a higher long-run rate would likely lead markets to price a shorter and shallower easing cycle to return policy to a more neutral stance, in turn posing a medium-term headwind for risk, and Treasuries.

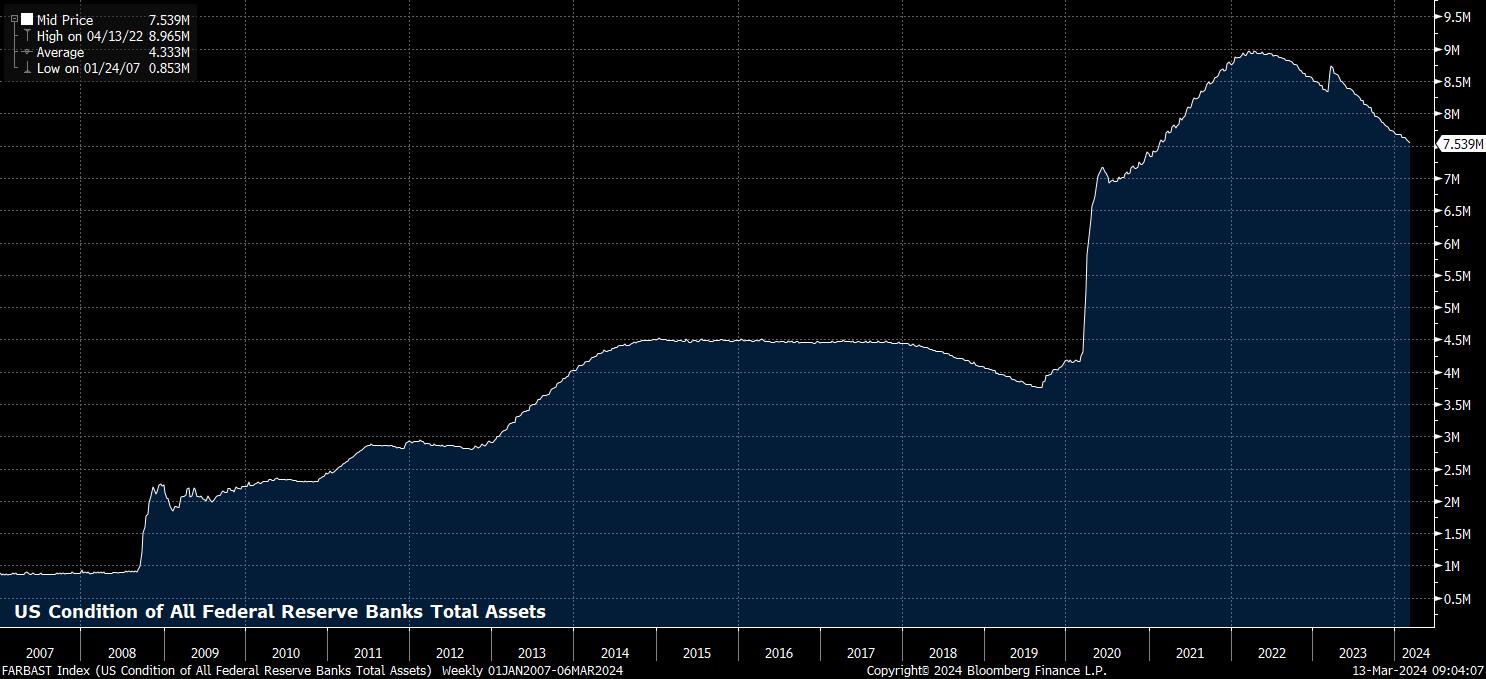

While the latest forecasts, and ‘dot plot’ will likely be the main highlights of the March decision, this month’s meeting will also mark the start of more formal, in-depth discussions on the tapering of the ongoing quantitative tightening (QT) process. It is probably premature, at this stage, to expect a formal decision on how QT will come to an end, though at present it seems likely that a QT taper announcement will come at the May meeting, with said taper beginning in June, particularly as overnight reverse repo usage continues to dwindle, and the volume of bank reserves moves ever closer to the ‘LCLoR’ (Lowest Comfortable Level of Reserves).

Turning to the post-meeting press conference, fireworks appear relatively unlikely.

Chair Powell most recently appeared on Capitol Hill at the beginning of March, and with said presser coming precisely a fortnight after said Congressional testimony, any remarks from Powell are likely to be, by and large, a repetition of what was said in front of lawmakers.

As a result, Powell is again set to stress that while it will “likely be appropriate” to cut rates this year, and that the FOMC will ‘carefully remove’ their current restrictive stance, both actions will hinge on the Committee obtaining “more confidence” on inflation moving back towards the 2% target.

Taking into account the lack of significant policy, guidance, or rhetoric shifts that are expected from the March FOMC, markets seem likely to take the decision in their stride, with the path of least resistance continuing to lead higher for both equities, and the dollar.

That said, risks to this view are present. Chiefly, there is the risk that the median 2024 dot implies just 50bp, rather than 75bp, of cuts this year; this would clearly lead to a hawkish cross-asset reaction, sparking downside in equities and Treasuries, and upside in the greenback.

More broadly, risks do appear tilted towards a hawkish fallout from the March decision, given that there is little, if anything, in the data at present to justify a further dovish pivot, and with markets already pricing an outlook in line with the current median dots.

Related articles

Pepperstone不保证这里提供的材料准确、最新或完整,因此不应依赖这些信息。这些信息,无论来自第三方与否,不应被视为推荐;或者买卖的要约;或者购买或出售任何证券、金融产品或工具的邀约;或者参与任何特定的交易策略。它不考虑读者的财务状况或投资目标。我们建议阅读此内容的任何读者寻求自己的建议。未经Pepperstone批准,不得转载或重新分发这些信息。