- Português

- English

- Español

- 简体中文

- 繁体中文

- Tiếng Việt

- ไทย

- لغة عربية

- Português

- English

- Español

- 简体中文

- 繁体中文

- Tiếng Việt

- ไทย

- لغة عربية

Análises

A Traders’ Weekly Playbook: Records are there for breaking

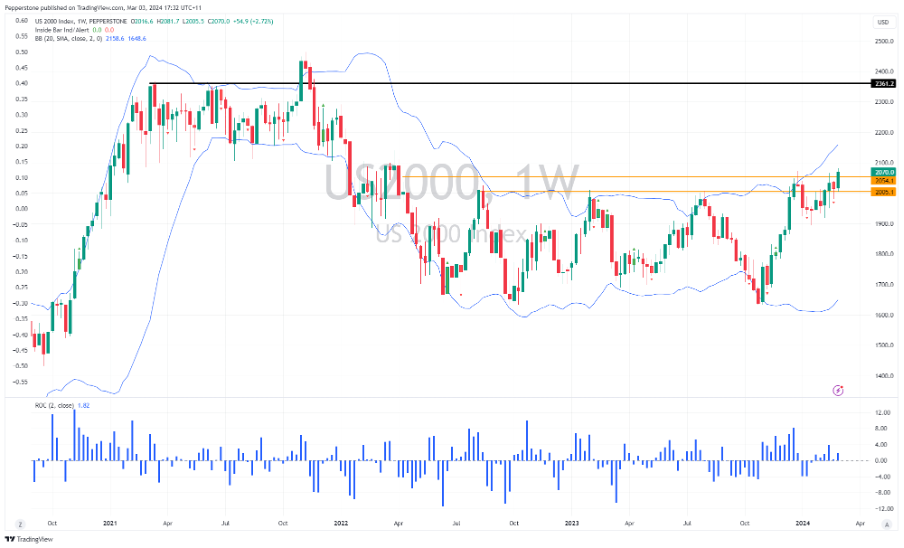

The result was new all-time highs in the US500, US30 and NAS100, with the US2000 eyeing a key breakout of its longer-term range high. New US equity highs backed new highs seen in the AUS200, JPN225 and EU Stoxx and GER40. Gold also got huge attention from clients, rallying 1.9% to set at a new closing high, and we’ve seen many in our alt-crypto offering (notably Bitcoin cash) ripping.

We’ll see if the feel-good factor lasts, but I find it interesting that equity and risky assets rallied despite seeing poor US data – where it’s easy to argue that poor data that increases economic slowdown risk, could have prompted risk aversion. So, while we can also point to Fed chatter, it seems in this case bad economic data was good for risk, with the overriding factor being increased rate cut expectations.

We’ll see if that same reaction is seen in the outcome of the US ISM services print and the various labour market readings, as these will be the key cross-asset drivers this week. Powell’s testimony to Congress will also get a look-in from traders and we know if he wants to move market pricing he can.

The ECB and BoC meeting and the China NPC meeting will get good attention but will play second fiddle to the US data.

The poor market internals in equity may be an amber warning sign to some, but market internals and breadth have offered no profitable signal for a while - pullbacks remain shallow and there is a hunt to go hard on risk. There is plenty to navigate this week but for now, the price action shows that the bulls are very much in control. Long equity hedged with gold exposures seems the play, and looking at the charts on the higher timeframes it feels like the path of least resistance being onwards and upwards.

Good luck to all.

The marquee event risks for the week ahead:

The key risk events for markets this week – China NPC meeting, ECB meeting, Jay Powell’s testimony to Congress & US nonfarm payrolls.

Monday

Switzerland CPI (18:30 AEDT) – the market looks for CHF headline CPI to print 1.1% yoy (from 1.3%) and core CPI at 1% (from 1.2%). The CHF swaps market prices a 25bp cut at the Swiss National Bank (SNB) meeting on 21 March at 70%, so a weaker than expected CPI print should see the market push that implied to c.90%, suggesting the SNB could lead G10 central banks in the sequencing of policy easing. As a result the CHF could become a consensus short from hedge funds. Look for XAUCHF to rally hard on a weak CPI number.

Tuesday

US ISM Services Index (Wednesday 02:00 AEDT) – the market looks for the services index to print 53.0 (from 53.4). Given the moves in risky assets (equity, credit) and gold post last week’s ISM manufacturing this data point could drive market volatility. A print below 51.0 would be a surprise and promote further upside in XAUUSD, with the market putting notable attention on the new orders and unemployment components of the survey.

Japan (Feb) Tokyo CPI (10:30 AEDT) – the market looks for JP headline CPI to print 2.5% (from 1.6%) and CPI ex-food and energy unchanged at 3.1%. After last week’s upside surprise in the JP national CPI print, and the upside move in 2-year JGB yields to 0.19% (the highest level since May 2011), the market will watch this one closely and an upside surprise could see JPY shorts cover.

BoJ Gov Ueda speaks at a fintech summit (15:00 AEDT) – after speaking last week at the G20 meeting and his comments considered dovish, we’ll see if this is the forum for a change in Ueda’s stance.

‘Super Tuesday’ – the biggest day in the primaries calendar, with some 15 states voting to nominate their choice of Presidential nominee. Given Trump’s result in South Carolina, it seems a done deal that he will get the REP nomination, so it's hard to see Super Tuesday as a market event.

China 14th National People Conference – the market will learn of the government’s economic targets for 2024 and what they are aiming for GDP, inflation, unemployment, and the deficit. We should see officials target growth of “around 5%” but it is feasible they aim for more.

Wednesday

US JOLTS job openings (Thursday 02:00 AEDT) – the market looks for 8.89m job openings (from 9.026m) – Traders with long positions in equity and gold and USD shorts will want to see a weaker print vs consensus expectations.

Australia Q4 GDP (11:30 AEDT) – the market looks for Q4 GDP of 0.3% QoQ / 1.4% YoY (from 2.1%), but expectations will be massaged as we get the partials (inventory, company profits, net exports as a percentage of GDP). Can’t see this being a mover of the AUD to any great degree, so would have limited concerns about holding AUD positions over this data point.

UK Budget (23:30 AEDT / 12:30 local) – Rishi Sunak needs Jeremy Hunt to pull a rabbit out of a hat to get voter momentum into the UK election - but one questions if this budget moves the dial on voting intentions and impacts the UK bond market, and by extension the GBP? Recent media suggests the chance of a major fiscal boost from the budget has been reduced - see my colleague Michael Brown's preview here.

Bank of Canada meeting (Thursday 01:45 AEDT) – the BoC won’t move on policy and will almost certainly keep rates at 5%. Given the recent downside surprise in December GDP (1.1% YoY) and January CPI print (of 2.9%) we could get stronger guidance on future easing. CAD swaps price 85bp of cuts (or just over three 25bp cuts) by December, so the move in the CAD will come as traders reconcile the tone of the statement with this pricing.

Thursday

Fed chair Jay Powell testifies to Congress (Friday 02:00 AEDT) – Jay Powell’s testimony will garner big attention from the market, where most see Powell offering a balanced/neutral view of economic risk and policy – this is his last formal forum to speak before the 20 March Fed meeting, in which some feel some risk of a risk of a hawkish pivot.

China trade data (no set time) – a hard one to react to given there is no set time for the release – the market looks for exports to increase by 3% and imports by 1.5%. A larger import number could boost currencies such as the AUD, NZD, and CLP.

Japan labour cash earnings (10:30 AEDT) – while we look ahead at Japan’s spring wage negotiations, the market looks for cash earnings of 1.3%, which suggests real wages of -1.4%

Mexico CPI (23:00 AEDT) – the market looks for headline CPI at 4.43% (from 4.88%) and core CPI at 4.62% (from 4.76%). Given recent economics, the prospect of a 25bp cut in the 21 March Banxico meeting looks likely, and the CPI print could reinforce that belief. Conversely, an upside surprise could see USDMXN break 16.9924 support and offer a larger downside move to 16.8000.

ECB meeting (Friday 00:15 AEDT) – the ECB are not expected to ease until June, so the statement and Christine Lagarde’s speech will most likely reflect the market’s central view. The bar seems high for the ECB to open the door to an April cut at this meeting, and Lagarde’s commentary may point to a “few month months” of data before they ease. The ECB’s updated economic projections, while likely to be downgraded, will still not be poor enough to suggest increased urgency to normalize. Unless we get a big surprise from the ECB, I’d be looking to fade moves in EURUSD into a 1.0920 to 1.0760 range this week.

Friday

US nonfarm payrolls (Sat 00:30 AEDT) – the market looks for moderation from the blowout January report, where the consensus sits at a healthy 200k jobs created in February. The unemployment rate is expected to remain at 3.7%, with average hourly earnings growing 4.3% yoy (from 4.5%). NFPs is the marquee event risk of the week, but forging a playbook is not clear cut – One questions if a rise in the U/E rate lifts risky assets as bond yields fall (rate cut expectations increase), or whether this outcome promotes risk aversion as traders consider the negative implications on economics. The USD will hold the cleanest read on the review of the data.

Canada employment report (Sat 00:30 AEDT) – the market looks for 20k jobs created and a tick up in the U/E rate to 5.8%.

International Women’s Day

Saturday

China CPI/PPI (12:30 AEDT) – the market sees CPI increasing by 0.2%, which would mark the first positive read after four months of falling consumer prices (month-on-month). PPI is eyed -2.6%. The trader’s concern here is around whether this offers any gapping risk for China assets, or its proxies (AUD, NZD, CLP etc) – I would argue it doesn’t.

US earnings – Target, Marvell Technology, Costco, Broadcom

Full Fed speaker line-up for the week

Related articles

O material fornecido aqui não foi preparado de acordo com os requisitos legais destinados a promover a independência da pesquisa de investimento e, como tal, é considerado uma comunicação de marketing. Embora não esteja sujeito a nenhuma proibição de negociação antes da divulgação da pesquisa de investimento, não buscaremos obter qualquer vantagem antes de fornecê-la aos nossos clientes. A Pepperstone não representa que o material fornecido aqui é preciso, atual ou completo e, portanto, não deve ser confiável como tal. As informações, quer sejam de terceiros ou não, não devem ser consideradas uma recomendação; ou uma oferta de compra ou venda; ou a solicitação de uma oferta para comprar ou vender qualquer título, produto financeiro ou instrumento; ou participar de uma estratégia de negociação específica. Não leva em consideração a situação financeira ou objetivos de investimento dos leitores. Aconselhamos aos leitores deste conteúdo que busquem seu próprio conselho. Sem a aprovação da Pepperstone, a reprodução ou redistribuição desta informação não é permitida.