- Italiano

- English

- Español

- Français

- Italiano

- English

- Español

- Français

Trader thoughts - the set-ups, event risks and moves you need to know

Direttore della ricerca

9 mar 2021

Share

Today we'll start with the US bond market as this is where the magic begins.

- Given the dynamic in the bond market gold has gained 2.0%, with silver up 3.5%. I've flagged a turn in gold off trend support, conditional on real yields moving lower. Well, price closed above the 5-day EMA (XAUUSD) however, with the event risk on the docket and the subsequent two-way risk in bonds, longs still lack conviction and I’d keep position sizing small. However, there's been some solid short covering.

- On the day we see better buying play out in the nominal Treasury curve, with the US 10-yr Treasury closing lower by 6bp at 1.52%. Real (adjusted for inflation expectations) Treasury yields are also lower, with 10s down 7bp. We’ve seen 4.5bp being priced out of the US rates market through to 2023 – this is key and broad markets have reacted as I discuss.

- Can bond yields go lower? Perhaps but key event risk looms ominously - US CPI (in US trade at 00:30 AEDT) will be closely watched, with expectations of 1.7% (from 1.4%) for headline CPI YoY. We also see the US Treasury auctioning $38b in 10yr Treasuries (5am AEDT) – if there is weak demand in the auction and a hotter CPI print, yields could easily go higher and this could set markets off. Good demand and weaker CPI and yields go lower.

- The US House will vote on the COVID-19 relief bill at 9:00am local time (1am AEDT). I suspect this is priced into the markets, but I also see limited scope for a fade the fact scenario to play out.

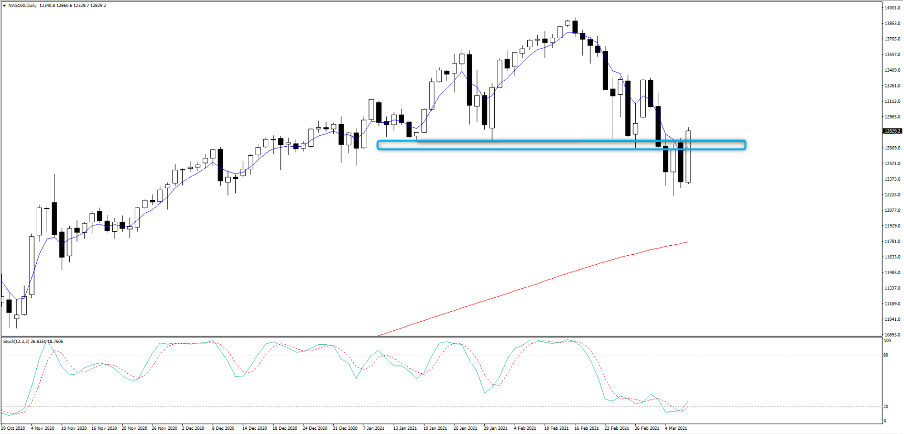

- Tech has flown. The NAS100 has printed two higher lows and closed through resistance into 12,780 and sits up a punchy 4.0% on the day. Value, while up on the day, has underperformed and there's been rotation into growth and tech. Again, is this a one-day affair? The bond market holds all the clues but 13,000 is the target followed by the 50-day MA at 13,147.

- Tesla has absolutely smashed it today, rallying nearly 20% - the best day since 3 Feb 2020. Volume is not as convincing as some would like (given the extent of the rally) at 66m shares traded, but it shows that a small move in bond yields can cause a huge move in this name.

- The USD sits -0.4% lower, but the declines are broad based. The big percentage moves on the day have been seen vs the ZAR, MXN, and SEK. EURUSD has found buyers into the 200-day MA at 1.1829, with the yield premium demanded to hold USTs over German bunds coming in 3bp and compelling EURUSD buyers.

- All eyes on the ECB (tomorrow 23:45 AEDT), so watch EUR exposures into this meeting - the market expects a dovish turn as the bank really don’t want tighter financial conditions, but will they meet dovish market expectations? I (perhaps optimistically) favour selling EURAUD rallies into 1.5480, with the pair getting a small boost after RBA gov Lowe speech this morning.

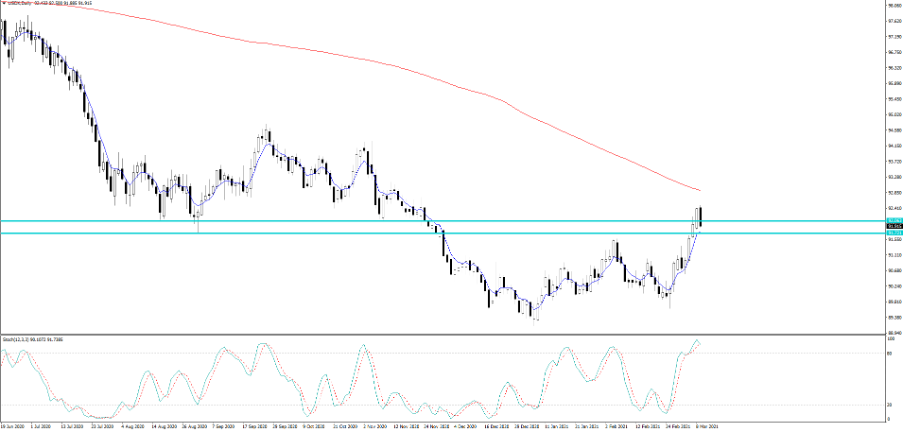

- The fall in yields has weighed on USDJPY, which has been sold almost to the pip at the 2015 downtrend. I favour buying weakness into 108.07, but again the fate of this pair hinges on the direction of the US bond market.

- USDCNH gets a strong focus today, as will the Chinese equity markets (trade the CN50 with us) given the recent declines and volatility. USDCNH is especially key for broad financial markets given the influence on reflation assets, such as commodities and there will be focus on China’s February CPI/PPI print at 12:30 AEDT (consensus -0.3% and 1.5% respectively). There'll also be a focus on Iron ore futures which traded nearly 6% lower yesterday.

- Bitcoin looks strong at 54,700 and it wouldn’t shock to see price make an assault on the February high of 58,350. Lots of talk of large buyers in size over $100k doing the rounds.

Charts to keep an eye on

(USDJPY daily)

USDX

NAS100

Iniziamo a fare trading?

Iniziare è facile e veloce. Con la nostra semplice procedura di apertura conto, bastano pochi minuti.

Il materiale qui fornito non è stato preparato in conformità con i requisiti legali volti a promuovere l'indipendenza della ricerca sugli investimenti e pertanto è considerato una comunicazione di marketing. Anche se non è soggetto a divieti di trattativa prima della diffusione della ricerca sugli investimenti, non cercheremo di trarne vantaggio prima di fornirlo ai nostri clienti.

Pepperstone non dichiara che il materiale qui fornito sia accurato, attuale o completo e pertanto non dovrebbe essere considerato tale. Le informazioni, sia da terze parti o meno, non devono essere considerate come una raccomandazione, un'offerta di acquisto o vendita, la sollecitazione di un'offerta di acquisto o vendita di qualsiasi titolo, prodotto finanziario o strumento, o per partecipare a una particolare strategia di trading. Non tiene conto della situazione finanziaria o degli obiettivi di investimento dei lettori. Consigliamo a tutti i lettori di questo contenuto di cercare il proprio parere. Senza l'approvazione di Pepperstone, la riproduzione o la ridistribuzione di queste informazioni non è consentita.

Pepperstone non dichiara che il materiale qui fornito sia accurato, attuale o completo e pertanto non dovrebbe essere considerato tale. Le informazioni, sia da terze parti o meno, non devono essere considerate come una raccomandazione, un'offerta di acquisto o vendita, la sollecitazione di un'offerta di acquisto o vendita di qualsiasi titolo, prodotto finanziario o strumento, o per partecipare a una particolare strategia di trading. Non tiene conto della situazione finanziaria o degli obiettivi di investimento dei lettori. Consigliamo a tutti i lettori di questo contenuto di cercare il proprio parere. Senza l'approvazione di Pepperstone, la riproduzione o la ridistribuzione di queste informazioni non è consentita.