- Italiano

- English

- Español

- Français

- Italiano

- English

- Español

- Français

Could stagflation be the smoking gun for higher volatility in markets?

The S&P 500 continues to be a central focus here, where as long as the index is above the 50-day MA we tend to see ‘buy the dip’ strategies working well. For example, in this dynamic when we’ve seen the 2-day RSI head below 10, it tends to be the trigger for mean reversion trades and the index has pushed back to the 10-day EMA 86.11% off the time.

*I have back tested S&P 500 futures, using data back to 2000 and this would have resulted in 108 trades being placed.

So, as long as price holds the 50-day MA then buying weakness is the way to go it seems.

(Source: Tradingview - Past performance is not indicative of future performance.)

We obsess on risk – mostly around what can go wrong, but also what can positively impact – it’s important to keep an open mind when trading discretionary. With that in mind, I, like many in the macro world, are watching the divergence between growth expectations, consensus earnings forecasts and ultimately price action. We know Q3 has been far weaker than many had expected with Delta playing into behaviours – that is not just in the US but globally – we’ve seen a few prominent economists and Morgan Stanley, Goldman’s and JPM cutting Q3 GDP estimates (due 28 October) well below the consensus call of 6%, with various Nowcast models seeing US Q3 GDP at 3.4% to 3.6%.

The view is that growth will snap back into Q4 and that Q3, therefore, marks the low point.

The street widely believes that Delta is close to peaking, and while there is a lag effect consumption should come roaring back. The idea of a lag is key because we ask whether we indeed do get a snapback in US payrolls at the 8 October meeting? Clearly this is key to cement a Fed taper in November/December. Most economists feel we will see a better jobs print – indeed, the price action in the bond market on Friday suggested investors saw last week’s payrolls impacted by factors that won’t be as prevalent in the September NFP (due 8 October).

But how long can the data roll in on the weaker side and traders continue to say “this was affected by Delta, Q4 will be better”.

Next week we get US PPI and CPI, and producer prices are expected to increase 40bp to 6.6% - we’ve seen a strong and positive response in wages, but we also know that central banks, notably the Fed, are watching unit labour costs (think remuneration/output) most closely. However, if business inputs are rising then inflation expectations will grind higher.

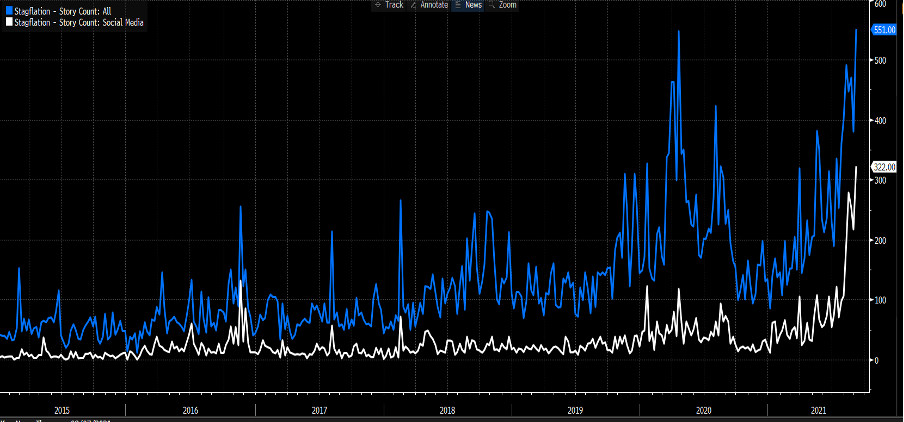

Blue – story count on Bloomberg, white – story count on social media

(Source: Bloomberg - Past performance is not indicative of future performance.)

In a world where inflation expectations are sticky and near-term growth expectations are slowing, the word ‘stagflation’ is being used far more liberally – there are plenty of articles that have pondered on the subject, in fact, running the story count we see articles on stagflation are through the roof - the idea of central banks normalising policy into an emerging environment of stagflation may not sit well with bond or equity investors.

If you sit in the camp that growth is due to snapback in Q4 then you’ll look through this period of Delta-induced economic weakness and not be overly concerned with stagflation. However, if Q4 numbers start to come down one has to believe S&P500 2021 consensus EPS of $2.02 and next year’s estimate of $2.21 could be at risk. Could that cause volatility to rise across asset class?

As long as the S&P500 holds the 50-day MA then buy the dip strategies should continue to work, but a close through the moving average and we may well see the markets talk themselves into a more pronounced drawdown. It’s cheap to own portfolio protection – maybe it's time to put the VIX index on the radar?

Related articles

Iniziamo a fare trading?

Iniziare è facile e veloce. Con la nostra semplice procedura di apertura conto, bastano pochi minuti.

Pepperstone non dichiara che il materiale qui fornito sia accurato, attuale o completo e pertanto non dovrebbe essere considerato tale. Le informazioni, sia da terze parti o meno, non devono essere considerate come una raccomandazione, un'offerta di acquisto o vendita, la sollecitazione di un'offerta di acquisto o vendita di qualsiasi titolo, prodotto finanziario o strumento, o per partecipare a una particolare strategia di trading. Non tiene conto della situazione finanziaria o degli obiettivi di investimento dei lettori. Consigliamo a tutti i lettori di questo contenuto di cercare il proprio parere. Senza l'approvazione di Pepperstone, la riproduzione o la ridistribuzione di queste informazioni non è consentita.