- Français

- English

- Español

- Italiano

- Français

- English

- Español

- Italiano

US CPI preview – a playbook for trading the marquee event risk on the calendar

The economist's median estimate (we consider to be the consensus) – core CPI is eyed at 0.4% Mom and 5.5% YoY (down from 5.7% in Dec), with headline CPI eyed at 6.2% (from 6.5%).

*The Cleveland Fed inflation nowcast model currently sits at 5.6% YoY.

Looking at options pricing I see higher implied volatility and expected movement for the US CPI print than any other economic data release – the market expects big movement. For traders these volatility events offer opportunity, but also, it’s a risk that needs to be managed, and we decide whether to add exposures over such events, hedge, reduce or even exit.

We manage risk – and depending on the strategy applied, we cut loss early, yet try to extract as much juice out of our winning trades as possible. The US CPI print is a risk and for those who can’t trade the late EU/US trading session, there are disadvantages to not being in front of the screens, so that one can react in real-time – this should be a consideration.

If we think about the psychology of the market and ultimately the expected direction in US inflation trends, it is one where CPI is expected to fall back towards the Fed’s target – core CPI is what the market is putting more weight on (over headlines CPI) and ultimately, it's going the right way.

However, anything that has us questioning that consensus vision would cause a shock, certainly from a positioning perspective, and as we all know uncertainty creates volatility.

So a hot CPI print would challenge that consensus view and the market position – especially when the Fed is openly warming to signs of a disinflationary period.

What is hot?

Any number which threatens the market consensus – so a 5.7% CPI print and indeed above would be enough to cause a big move higher in the USD, and cause growth equity (such as NAS100/tech), the AUD, and gold to be hit. A number above 5.7% would be a surprise and naturally, the higher that print proves to be, the greater the extent of the move lower in risky assets.

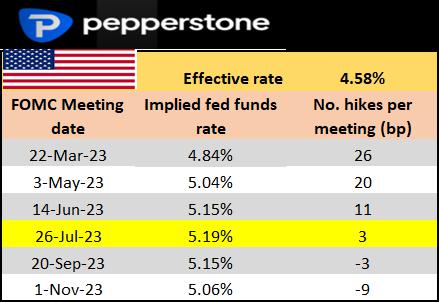

Rates review – what’s priced into the interest rates market – we look at the pricing for the next FOMC and the step up (in basis points) per meeting.

*The line highlighted in yellow represents peak fed pricing

A big number should see the implied probability of a 50bp hike in the 22 March FOMC meeting rise to c.30-40%. We’d see the peak fed funds pricing move from 5.19% to a 5.25%-5.30% range. The USD would rally hard, and risk assets, such as NAS100, crypto and AUD would fall hard.

What is weak?

If the consensus is on the money, then this would be the fourth fall in a row where YoY price pressures have eased – the market's projected path for inflation is validated, and we all breathe a sigh of relief.

With that in mind, the market may offer some margin of error on an upside surprise, that is, if the print is lower than 5.7% (last month’s print) – of course, we’ll look at the components within the CPI basket and look for trends that offer a higher probability of a change in direction in price pressures. – but while a CPI print around 5.5% to 5.6% is above consensus, it is still a fall, and therefore traders may look to sell rallies in the USD.

A print below 5.4% would be a surprise and should see rate hike expectations for the March FOMC fall from 26bp to 20bp and peak pricing for Fed hikes pulling back to around 5%. Here, the USD would fall, most prominently vs the NOK, AUD, and NZD. Gold and commodities would rally and the NAS100 would rally strongly.

USDJPY would be interesting as this comes on the same day as the new BoJ governor nominees are announced – so the JPY may have its own issues to work through.

In times like this we ask - where is the pain trade? I’d argue the market would be more surprised by an upside surprise than a downside surprise – the real pain would come if inflation didn’t fall and stayed at 5.7%. Those not short risk in any great capacity is desperate to see the vision of lower inflation take hold – let's see if it plays out.

Le matériel fourni ici n'a pas été préparé conformément aux exigences légales visant à promouvoir l'indépendance de la recherche en investissement et est donc considéré comme une communication marketing. Bien qu'il ne soit pas soumis à une interdiction de traiter avant la diffusion de la recherche en investissement, nous ne chercherons pas à tirer parti de cela avant de le fournir à nos clients. Pepperstone ne garantit pas que le matériel fourni ici est exact, actuel ou complet, et ne doit donc pas être utilisé comme tel. Les informations, qu'elles proviennent d'un tiers ou non, ne doivent pas être considérées comme une recommandation; ou une offre d'achat ou de vente; ou la sollicitation d'une offre d'achat ou de vente de toute sécurité, produit financier ou instrument; ou de participer à une stratégie de trading particulière. Cela ne tient pas compte de la situation financière des lecteurs ou de leurs objectifs d'investissement. Nous conseillons à tous les lecteurs de ce contenu de demander leur propre conseil. Sans l'approbation de Pepperstone, la reproduction ou la redistribution de ces informations n'est pas autorisée.