- English (UK)

- English (UK)

Analysis

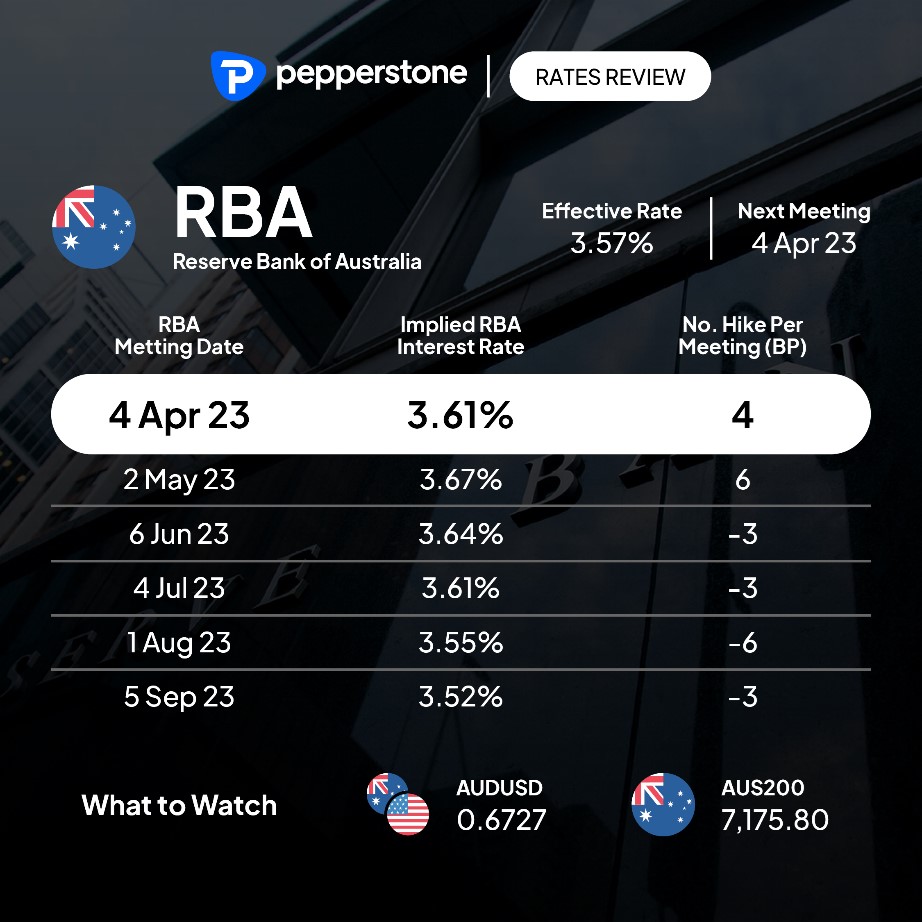

In the March RBA meeting minutes, the RBA noted policy was now in restrictive territory and they would “reconsider” the case for a pause in the April meeting. Is there enough new information to compel this pause?

Market expectations - hike or a pause?

The market prices just 4bp of hikes for this meeting, equating to a 16% chance of a 25bp hike. We see just 10bp of hikes priced for both the April and May meeting, with the market seeing the effective cash rate at 3.52% by September.

Economists’ expectations are more divided than the pricing implied in the interest rate futures – of 26 economists polled by Bloomberg 16 are calling for a pause and 10 for a 25bp hike.

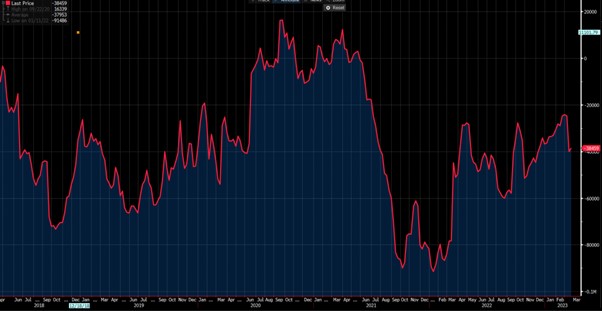

AUD positioning – essential when assessing risk around any major announcement.

Looking at AUD futures positioning, or spot FX positioning reported by banks, there is no extreme bias - so positioning, in isolation, shouldn’t result in any exacerbated moves in the AUD.

In the weekly CoT report, we see non-commercial accounts (trading FX futures) hold a net position of -38,459 contracts - that is the 49th percentile of the 5-year range. In the more defined TFF report leveraged funds (again trading FX futures) are small net long at 6290 contracts, the 67th percentile of the 5-year range.

(CFTC/CoT report – non-commercial AUD futures positions)

Investment bank flow reports portray leveraged funds running a small net short AUD position, while real money accounts are long but not neither are at extremes.

Pepperstone’s clients hold a net long AUD position, and this could be representative of broad retail trader positioning and sentiment.

Digging into this we see a split on the near-term direction of AUDUSD, with 52% of open positions held short (48% long). There is a more concentrated long bias in the AUD crosses with 77% of open positions in AUDNZD held long and 74% short EURAUD and 79% short GBPAUD. This is likely a reflection of the set-up in the pairs and not on the RBA meeting per se.

Trading the RBA meeting

Initial thoughts

I think the RBA holds rates unchanged, but I also think 4bp of hikes that are priced is too low and the probability of a hike should be closer to 40% than the implied 16%.

The downside in AUD on a pause seems limited, given the RBA will likely make it clear in the statement they will retain the flexibility to hike rates in May.

My preferred tactical approach is to fade any extreme initial moves – using limit orders to sell rallies or buy weakness, as I see a high probability the RBA statement may counter any initial move driven by their actions with the cash rate.

Need to know

Market pricing portrays a high degree of conviction that the RBA are on hold - so a 25bp hike could cause the AUD to see a solid spike off the bat. The extent by which price could extend would be driven by the RBAs statement and whether the market felt the wording suggested the May meeting was also priced too low.

With 10bp of hikes priced for both this meeting and May, the market is essentially saying that if they don’t hike at this meeting then it's unlikely the RBA will hike in May – this seems fair, as they are more likely to hike now and pause in May.

With subdued levels of AUD implied volatility, the market is not expecting to be shocked – for a genuine surprise I suspect we’d need to see a ‘dovish hold’ – where the RBA keep rates on hold and offers a clear view they will pause for an extended period as they assess the lag effect of tightening into the real economy. This seems unlikely given inflation is still far too high.

Conversely, a ‘hawkish hike’ – where we get a 25bp hike, and the statement signals another could come in May – this would get the AUD firing. Again, this seems unlikely, as it would cause a strong tightening of financial conditions at a time when growth is delicately poised.

The case for a hike - Those calling for a hike of 25bp see a tight labour market, strong business confidence, and high-capacity utilization. Digging into the Feb monthly CPI indicators we saw broad-based month-on-month rising price pressures – it was only holiday, travel and accommodation and recreation that created the disinflation impulse.

The case to pause - Those calling for the RBA to hold rates at 3.6% acknowledge that headline inflation is moderating quicker than expected, suggesting a big downside risk in the Q1 CPI print (released 26 April). There is clear evidence that inflation has peaked and fallen to the RBA’s estimate of 6.7% by June. Wage growth is not problematic and there are lag effects from 360bp of hikes that still need to filter through to the real economy – there is also a significant number of fixed-rate mortgages rolling off in Q223.

I think the RBA hold but I also see the implied probability too low – how do you see the risks?

The material provided here has not been prepared in accordance with legal requirements designed to promote the independence of investment research and as such is considered to be a marketing communication. Whilst it is not subject to any prohibition on dealing ahead of the dissemination of investment research we will not seek to take any advantage before providing it to our clients.

Pepperstone doesn’t represent that the material provided here is accurate, current or complete, and therefore shouldn’t be relied upon as such. The information, whether from a third party or not, isn’t to be considered as a recommendation; or an offer to buy or sell; or the solicitation of an offer to buy or sell any security, financial product or instrument; or to participate in any particular trading strategy. It does not take into account readers’ financial situation or investment objectives. We advise any readers of this content to seek their own advice. Without the approval of Pepperstone, reproduction or redistribution of this information isn’t permitted.